Why Hail Claims Fail: 7 Mistakes Contractors Make Before the Adjuster Shows Up

March 12, 2026

Written by Taylor Bezek

Share

Pre-inspection prep is where most hail claims are quietly decided. By the time the adjuster walks the roof, the clock has been running—and in many cases, it’s already run out.

- Most hail claim failures trace back to documentation and timing errors made before the adjuster ever arrives.

- Contractors who approach the adjuster inspection with a prepared data package consistently achieve better outcomes for clients.

- Understanding basic policy language and storm data isn’t optional—it’s the baseline for protecting your client and your scope.

- JustClaims partners with contractors to fill these gaps with data, preparation, and claims expertise.

Mistake 1: Waiting Too Long After the Storm

Most property insurance policies include a “prompt notice” or “timely reporting” requirement. What constitutes “timely” varies by policy and state, but the risk is real: carriers have denied claims—or reduced settlements—based on delayed reporting. More practically, storm evidence degrades. Granule deposits wash away. Impact marks weather. Photographs taken 90 days post-storm carry far less weight than those taken the week of the event.

The fix: Establish a storm response protocol. When a significant hail event hits your market, proactively contact clients in the affected area within 48-72 hours. Conduct a preliminary inspection and document conditions immediately—before any cleaning, patching, or debris removal.

Mistake 2: Not Pulling Independent Storm Data Before the Inspection

Walking into an adjuster inspection without independent storm data is like going to a negotiation without knowing the market price. The carrier’s adjuster has access to internal hail data—and it may not match publicly available records. Without your own data source, you’re debating opinion against opinion.

The fix: Before any adjuster inspection, pull a storm data report for the specific event date and parcel address. Know the hail size, storm path, and impact density before anyone steps on the roof. JustClaims provides this as a standard component of our contractor partnership program.

Mistake 3: Failing to Document Before Any Work Begins

This one should go without saying—but it still costs contractors and clients money every storm season. Emergency repairs, tarping, debris removal: all of these are necessary and appropriate. But if they happen before thorough photo and video documentation, you’ve potentially compromised your own evidence.

The fix: Document everything before touching anything. Full roof photo sets, close-up impact documentation per square, gutter condition, fascia, siding, skylights, HVAC equipment, and any auxiliary structures on the property. Use a consistent grid-based photo protocol so nothing gets missed and every image has a clear reference point.

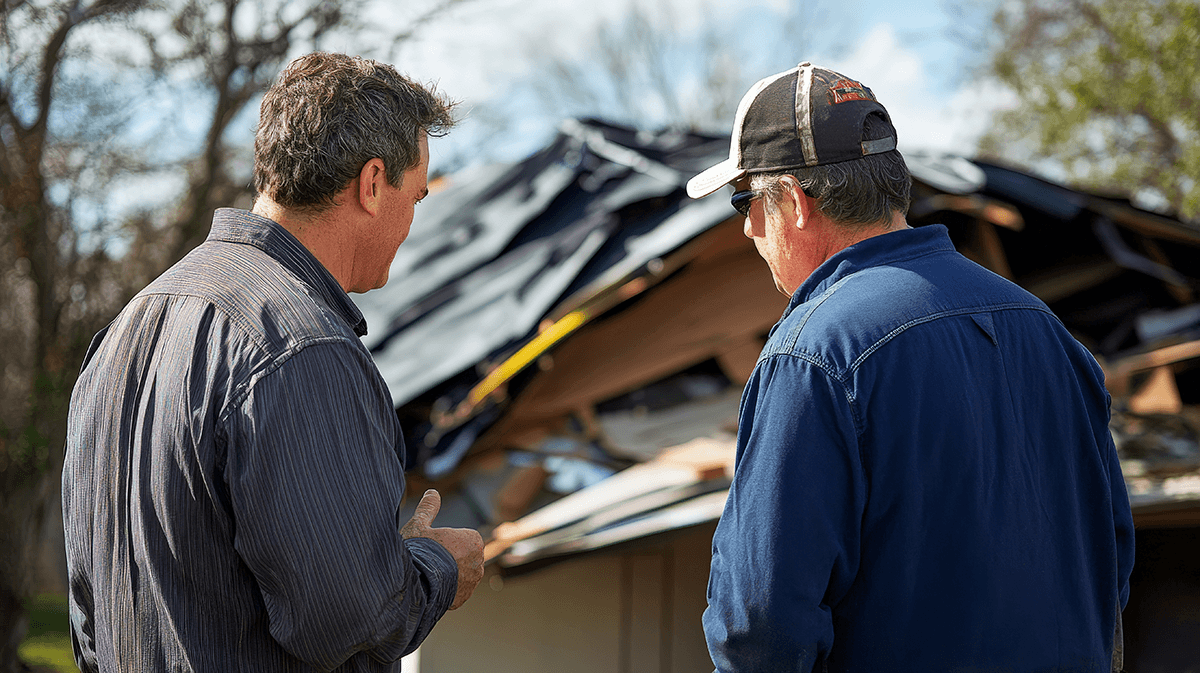

Mistake 4: Letting the Adjuster Inspect Alone

An adjuster conducting a solo inspection is an adjuster who controls what gets documented. When you’re not present, damage that’s awkward to include gets excluded. Notes about “prior condition” get written. The back slope gets a quick look instead of a full inspection. This is not hypothetical—it happens on a majority of claims where contractors aren’t present during the carrier inspection.

The fix: Always attend the adjuster inspection. If scheduling makes that impossible, send a trained representative. Bring your own inspection documentation and be prepared to walk the adjuster through specific damage areas, pointing to data that supports each line item.

Mistake 5: Ignoring Adjacent Structures and Systems

A hail claim is not just a roof claim. A significant hail event impacts every exterior surface: siding, windows, gutters, downspouts, skylights, HVAC condensers, solar panels, fencing, outbuildings, and detached garages. Adjusters often write the main roof and stop. Contractors who catch everything—and document it—protect their client’s full entitlement.

The fix: Build a comprehensive inspection checklist that covers every exterior component. Train your team to inspect every surface exposed to the sky during the storm. For commercial properties, this includes rooftop mechanical units, metal coping, flashing systems, and skylights—all of which can be impacted and all of which are frequently missed.

Mistake 6: Not Reading the Policy Before the Inspection

Going into an adjuster inspection without understanding the policy is like playing poker without knowing the rules. Lets be clear, reading and understanding a policy is not acting as a public adjuster without a license. Interpreting or explaining coverages/endorsements on behalf of an insured to their carrier is.

Does the policy have a cosmetic exclusion? Does the policy afford full RCV coverage? Are there matching requirements for adjacent undamaged materials? Is there a wind/hail deductible that changes the calculus entirely? These answers lend a better understanding on whether a proposed repair will be covered, as well as the insureds financial responsibility in getting them done.

The fix: Request a copy of the full policy, including all endorsements and riders, before the inspection. If the client doesn’t have it, help them request the declarations page and endorsements from their carrier. If the policy language is unclear, a quick consultation with JustClaims can translate it into a practical inspection and documentation plan.

Mistake 7: Treating the First Estimate as Final

The first estimate is an opening offer, not a verdict. This is perhaps the most expensive misunderstanding in the contractor-claims relationship. Adjusters make mistakes. Line items get missed. Pricing gets undervalued. Supplements exist precisely because first estimates are routinely incomplete—and filing a supplement is a normal, expected part of the claims process, not an act of aggression.

The fix: Review every carrier estimate line by line.. Compare it against your own scope of work. Identify missing line items, underpriced materials, and excluded structures. If the gap is significant, file a supplement with supporting documentation. If the carrier disputes the supplement, that’s what the appraisal process exists to resolve.

In Summary

None of these mistakes require expertise to avoid—they require preparation and the right partners. The contractors who consistently deliver for their clients aren’t the ones who know the most about roofing. They’re the ones who show up prepared, documented, and backed by data.

💬 Want a pre-inspection preparation checklist built for your market? Our contractor partners get access to the full JustClaims field toolkit.