2026 Colorado Wildfire Claims: Property & Smoke Loss Guide

May 14, 2026

Written by Taylor Bezek

Share

In Colorado, 74% of property owners affected by recent catastrophic wildfires found themselves severely underinsured, exposing a massive financial gap between their policy limits and actual rebuilding costs. Navigating a wildfire insurance claim requires strict documentation, proactive evidence gathering, and a deep understanding of state-specific coverage mandates. Protecting your financial recovery means treating your insurance claim as a rigorous legal process from day one.

Key Takeaways

- Underinsurance rate: 74% of Marshall Fire policyholders were underinsured.

- Severe coverage gaps: 36% of policies covered less than 75% of the actual rebuild cost.

- ALE duration: Colorado law mandates a minimum of 24 months of Additional Living Expenses coverage.

- Payment timeline: Insurers must pay for loss of use within 20 days of receiving documentation.

- Smoke damage limits: The Colorado Division of Insurance prohibits sub-limits that reduce coverage for smoke and ash damage.

Room-by-room video inventory — why you need it BEFORE a fire

Statutory Minimums Without Proof

In Colorado, insurers are required to pay 65% of personal property limits without a written inventory for total losses from a wildfire disaster at owner-occupied residences [1]. The primary burden of proof rests on the policyholder to demonstrate the value of losses above the statutory minimum payment, making pre-disaster documentation a critical component of financial recovery. Relying solely on this baseline payout often leaves families with a fraction of what they need to replace their belongings.

Best Practices for Documentation

The Colorado Division of Insurance advises property owners to maintain a comprehensive list of possessions, including purchase prices, model numbers, and serial numbers, as insurers will ask for proof of purchase when a claim is filed [2]. Creating a video inventory of personal property with an audio narration detailing brand names, purchase locations, and estimated costs can save significant stress and work after a loss [1]. When documenting contents, property owners should pull items out of drawers, closets, and cabinets to spread them out for more complete and accurate images [1]. Adjusters cannot compensate you for items hidden from view in a video, so thoroughness during the recording process directly impacts your final settlement.

Hidden smoke, ash, and soot as physical damage — often covered even if home did not burn

Regulatory Classification of Smoke

Because underinsurance and denied claims frequently stem from disputes over what constitutes physical destruction, understanding how the state treats secondary wildfire effects is critical for your financial recovery. The Colorado Division of Insurance officially classifies wildfire smoke, soot, ash, odor, and char damage as direct extensions of wildfire damage [3]. Even if the flames never touched your property, the infiltration of toxic particulates into HVAC systems, insulation, and porous materials constitutes legitimate physical damage that requires professional remediation.

Prohibition of Sub-Limits

Insurance companies historically attempted to minimize these payouts by burying restrictive clauses in policy language. In October 2025, the Colorado DOI issued Bulletin No. B-5.53, directing insurers to refrain from imposing sub-limits that reduce coverage for smoke and ash damage in residential property policies [4]. Regulators emphasized that capping payouts for smoke and soot contamination undermines the essential protection that Colorado policyholders reasonably expect from their insurance [5]. Debris removal coverage limits vary by policy and may be exhausted by toxic ash and foundation removal costs before rebuilding begins. This regulatory stance ensures that property owners have the financial backing necessary to conduct deep environmental cleaning and structural deodorization without hitting arbitrary coverage ceilings.

The Replacement Cost Trap in 2026 Colorado construction costs

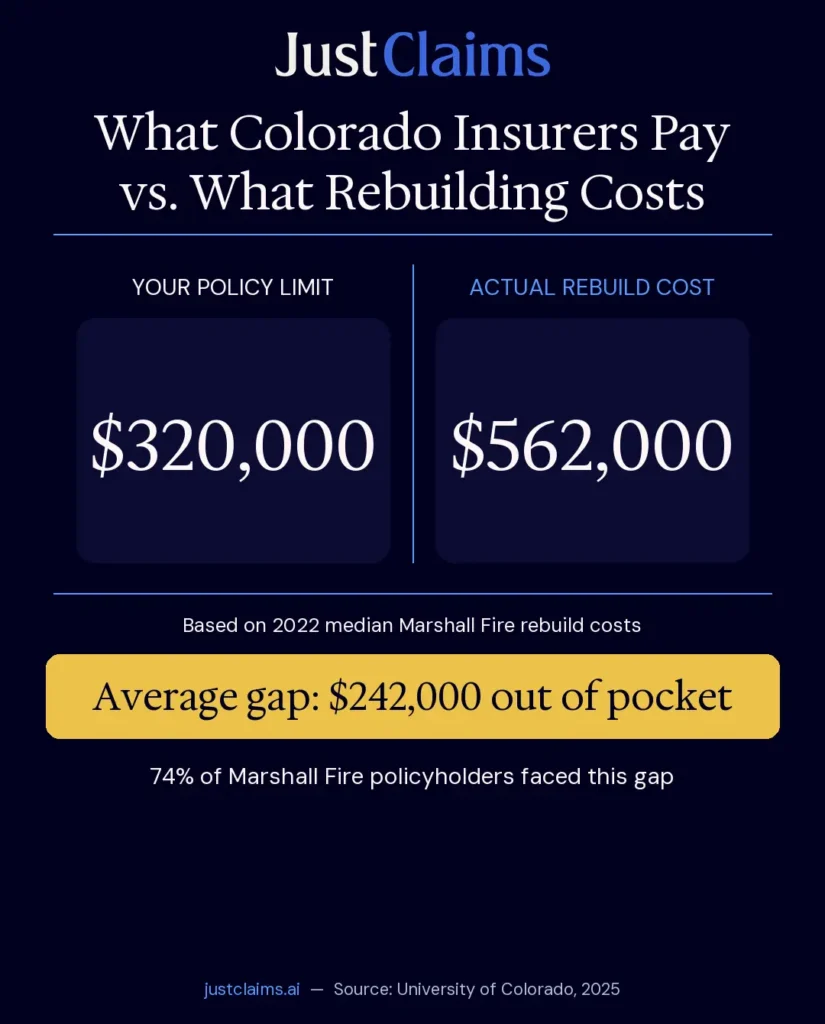

The Marshall Fire Underinsurance Crisis

Just as smoke damage disputes can derail a claim, the soaring cost of local construction frequently leaves property owners facing massive out-of-pocket expenses due to outdated policy limits. 74% of property owners affected by the Marshall Fire were underinsured, with 36% holding policies that covered less than 75% of the actual rebuild cost [6].

This crisis highlights a systemic failure in how properties are valued at the time of policy renewal, often ignoring the realities of post-disaster demand surge, supply chain bottlenecks, and inflation in building materials.

The Failure of Extended Replacement Cost

Many assume that wealth or premium policy endorsements provide immunity from these shortfalls, but the data proves otherwise. Underinsurance affects high-income earners as well; 72% of households with incomes above $180,000 held policies that did not cover the cost of a complete rebuild [6]. Furthermore, while 87% of the Marshall Fire policies studied included extended replacement cost coverage, nearly three-quarters of them still fell short of covering the full cost to rebuild [6]. Property owners must proactively review their Coverage A limits annually with local contractors, rather than relying on the insurance company’s automated valuation software.

Colorado-specific: the Division of Insurance complaint process if adjuster lowballs you

Initiating a DOI Investigation

When the replacement cost trap or denied smoke claims lead to unacceptable settlement offers, leveraging the state’s regulatory oversight becomes your primary mechanism for dispute resolution. The Colorado Division of Insurance (DOI) Consumer Services Team investigates complaints regarding property insurance and can be contacted at 303-894-7490 or DORA_Insurance@state.co.us to discuss issues before filing a formal complaint [7]. Engaging with the DOI early can provide clarity on whether your insurer’s actions violate state claims-handling regulations.

Navigating the Consumer Portal

Formal complaints must be submitted through the DOI’s secure Consumer Portal, which requires users to create an account to file the complaint, upload supporting documents, and communicate directly with the Division [7]. After successfully submitting a complaint through the portal, consumers receive a ‘Complaint ID’ and will be notified via email whenever there is activity or a response from the Division requiring their attention [7]. Accuracy and factual documentation are paramount when escalating a dispute — complaints should reflect your own account of events and policy details. [7]. Accuracy and factual documentation are paramount when escalating a dispute.

Additional Living Expenses (ALE) — what qualifies and how long it lasts

Understanding Coverage D Benefits

While fighting for fair property valuations through the state complaint process, securing your temporary housing benefits is essential to maintaining financial stability during a prolonged displacement. Additional Living Expenses (ALE), also known as Coverage D or Loss of Use, is designed to assist policyholders when their property is a total loss or rendered uninhabitable due to damage [8]. This coverage bridges the gap between your normal living expenses and the increased costs of temporary housing, extra commuting miles, and dining out while your kitchen is inaccessible.

Statutory Timelines and Extensions

Under Colorado law (C.R.S. 10-4-110.8), property insurance policies must provide ALE coverage for a minimum of 24 months, with the option to extend it twice by six months if there are delays in reconstruction or permitting [9]. Insurers in Colorado are required to pay for the loss of use of an insured property within 20 days of receiving documentation, such as a signed lease for temporary housing [9]. In the event of a catastrophic disaster, Colorado regulations require insurers to waive any waiting periods related to ALE benefits for policyholders whose properties need repair or replacement [10].

Frequently Asked Questions

How do I file a wildfire insurance claim in Colorado?

Immediately contact your insurance provider to initiate the claim process and request an advance on your Additional Living Expenses (ALE) if you are displaced. Document all damage with photos and video, keep every receipt for temporary housing, and contact the Colorado Division of Insurance if you believe your claim is being mishandled.

What happens if my insurance payout does not cover the cost to rebuild?

If your policy limits fall short of current construction costs, you may be responsible for the difference out of pocket. It is crucial to review your policy for extended replacement cost coverage, though data shows that even with these extensions, many property owners still face significant financial gaps.

Does my policy cover smoke damage if the fire did not reach my property?

Yes, the Colorado Division of Insurance classifies smoke, soot, ash, and odor as direct extensions of wildfire damage. State regulators have directed insurers not to impose sub-limits that reduce coverage for these specific types of contamination.

How long will my insurance pay for temporary housing?

Colorado law mandates that policies provide Additional Living Expenses (ALE) coverage for a minimum of 24 months. This duration can potentially be extended twice by six months if you experience unavoidable delays in reconstruction, permitting, or contractor availability.

The Bottom Line

Recovering from a wildfire requires more than just filing paperwork; it demands a proactive approach to documenting losses, understanding state-mandated coverage minimums, and holding insurers accountable to Colorado regulations. From securing immediate Additional Living Expenses to navigating the complexities of smoke damage and replacement costs, property owners must treat their insurance claim as a rigorous financial transaction.

Falling into the underinsurance trap or accepting a lowball settlement can jeopardize your ability to rebuild your life. By maintaining detailed inventories, leveraging the Colorado Division of Insurance’s complaint process when necessary, and understanding your rights regarding secondary damage, you can better protect your financial future. Upload your claim documents to JustClaims to see in minutes if your insurer missed coverage you’re owed.

This content is for informational purposes only and does not constitute legal or insurance advice.

Sources

[1] https://cl.cobar.org/features/proving-covered-personal-property-loss-under-a-homeowners-policy/

[4] https://aaisviews.aaisonline.com/compliance-alerts/colorado-bulletin-wildfire-damage-sub-limits

[5] https://www.propertyinsurancecoveragelaw.com/blog/colorado-smoke-and-soot-coverage-bulletin/

[7] https://doi.colorado.gov/for-consumers/file-a-complaint

[8] https://doi.colorado.gov/announcements/marshall-fire-response-faqs-on-additional-living-expenses-ale

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. A licensed Public Adjuster in TX (#2125659), FL (#W455048), CO (#769172), and 10 additional states, Taylor founded his own firm before joining JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor's mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.