Kentucky’s HB 568 Is Restricting Your Right to a Claims Advocate — Here’s What’s at Stake

May 11, 2026

Written by Ashley McMurry

Share

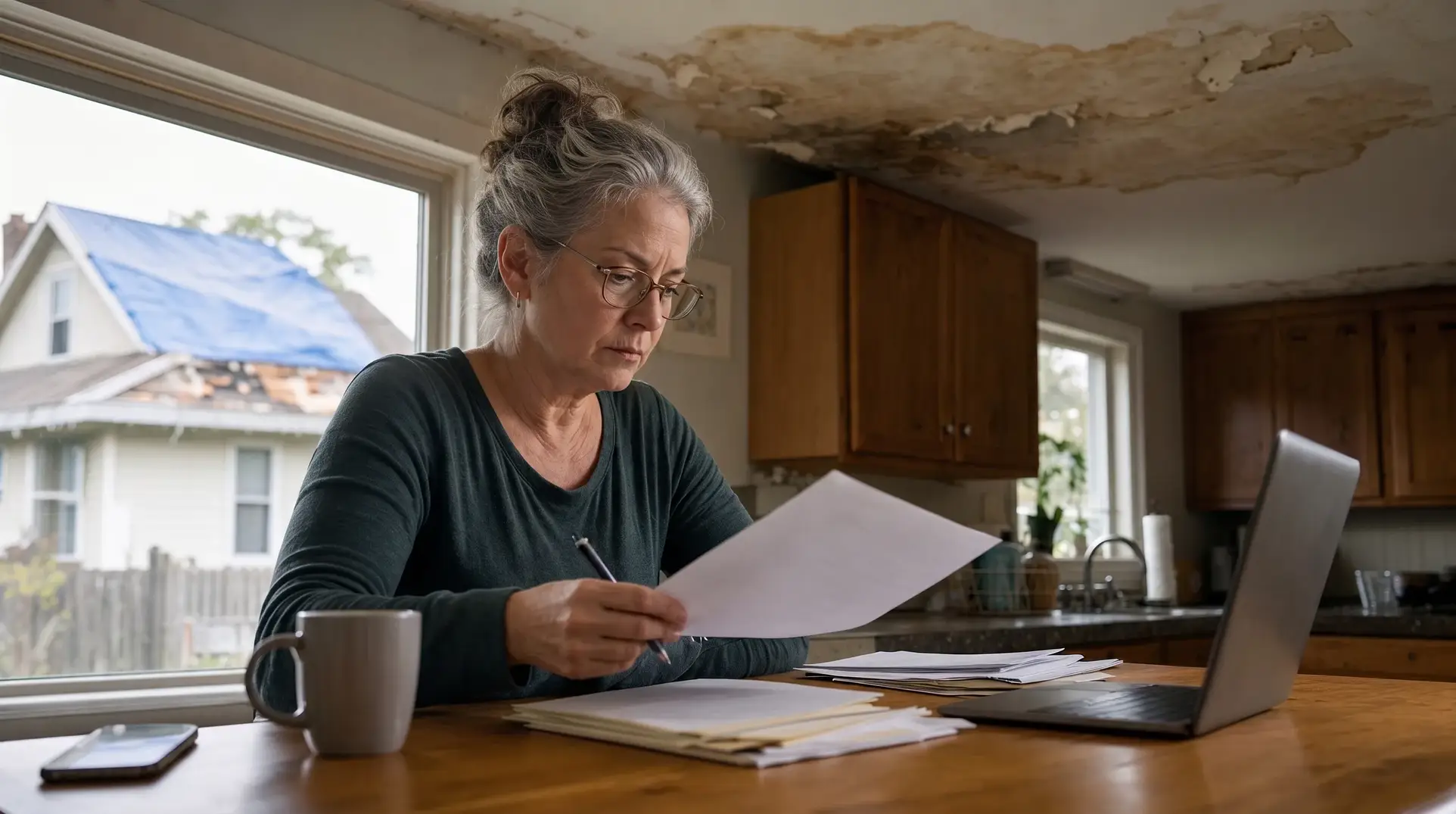

Kentucky just passed a law that makes it harder for policyholders to get professional help after a devastating insurance loss. If you’ve ever wondered who’s actually in your corner when you file a claim — and who isn’t — House Bill 568 makes that question more urgent than ever.

Key Takeaways

- What it is: Kentucky HB 568 is a 2025 law placing new restrictions on public adjusters — the licensed professionals who represent policyholders in insurance claims

- What it does: Prohibits claims advocates from contacting policyholders during blackout periods following disasters, caps professional fees, and adds administrative hurdles that deter experienced practitioners from complex cases

- Who it affects: Kentucky homeowners and property owners filing claims under residential and commercial property policies

- The legal challenge: HB 568 has already drawn a formal legal challenge, with opponents arguing the law unconstitutionally favors insurer interests over policyholder rights

- Why it matters nationally: Kentucky is not alone — similar legislative efforts have appeared in other states, making this a bellwether fight for policyholder access to professional representation

What Is a Public Adjuster — and Why Does the Name Matter?

A public adjuster is a licensed professional who works exclusively on behalf of the policyholder when filing an insurance claim. When your home is damaged by fire, flood, or a storm, your insurance company sends their own adjuster to assess the loss. That adjuster works for the carrier. A public adjuster — increasingly referred to in the industry as a claims advocate — is your independent expert, hired by you, accountable to you, and focused entirely on maximizing your recovery under your policy.

Think of it this way: if you were sued, you wouldn’t show up to court and rely on the opposing party’s attorney to represent your interests. Insurance claims work the same way. Both sides bring expertise to the table. A claims advocate is yours.

The terminology matters more than it might seem. The word adjuster is used for both the insurer’s representative and the policyholder’s representative — a source of real confusion that leaves many homeowners believing they’re already represented when they aren’t. Someone told us recently they had “already used an adjuster” — sent by the carrier. That confusion costs policyholders money. Claims advocate better reflects what these professionals actually do: they advocate for you.

As Forbes recently noted in a guide to public adjusters, policyholders who work with professional representation consistently achieve higher settlements than those who navigate the process alone — not because insurers are necessarily acting in bad faith, but because claims are complex, and expertise matters. ¹

What Does Kentucky HB 568 Actually Do?

Kentucky House Bill 568, passed in the 2025 legislative session, introduces a sweeping set of new restrictions on public adjusters operating in the state. Supporters framed the law as consumer protection. Critics — including the licensed professionals it directly regulates and the policyholders they serve — argue the practical effect is to limit access to expert representation at exactly the moments homeowners need it most.

The law arrived alongside a broader national pattern of insurer-backed legislation targeting the public adjusting profession. Kentucky’s version is among the more aggressive, and its passage has already triggered a formal legal challenge ahead of a legislative hearing. ²

The 4 Biggest Restrictions Under HB 568

1. Solicitation Blackouts After Disasters — When Help Is Needed Most

HB 568 prohibits public adjusters from contacting policyholders during defined blackout periods following a declared disaster. The intent, proponents say, is to prevent high-pressure solicitation of vulnerable homeowners in the immediate aftermath of a loss.

The problem: disasters are precisely when policyholders are most at risk of accepting an inadequate settlement. In the days after a tornado, flood, or fire, insurers move quickly. Their adjusters are already in the field. Delaying a policyholder’s access to their own professional representative doesn’t protect them from pressure — it simply removes a counterweight to it.

Bad actors in the industry should be addressed through existing licensing and conduct standards. A blanket blackout on all contact isn’t a scalpel — it’s a blunt instrument that penalizes ethical practitioners and leaves policyholders underrepresented during the most critical window of their claim.

2. Fee Caps That Push Experienced Professionals Out of Complex Cases

The law establishes caps on the contingency fees public adjusters can charge. On their face, fee limits sound reasonable. In practice, they create a distorted market.

Public adjusters are typically paid a percentage of the final claim settlement — nothing unless they recover money for the client. Fee caps set too low make it economically unviable for experienced professionals to take on large, technically complex cases: the exact cases where a claims advocate’s expertise creates the most value for a policyholder. The result is that the policyholders with the most complicated losses — and the most to gain from professional representation — may find it hardest to attract qualified help.

3. Added Licensing Burdens That Disadvantage Independent Practitioners

HB 568 introduces new administrative and licensing requirements that add compliance costs and complexity. For large firms with dedicated legal and compliance staff, these are manageable. For smaller, independent claims advocates — many of whom are solo practitioners or small partnerships built on deep local expertise — they represent a meaningful barrier.

This consolidation pressure doesn’t serve policyholders. Local practitioners often bring granular knowledge of regional construction costs, local contractor markets, and community-specific claim patterns that national firms cannot replicate. Regulations that push them out of practice narrow the field of available advocates in ways that ultimately hurt consumers.

4. Contract Restrictions and Cooling-Off Periods That Slow Access

The law establishes cooling-off periods and contract restrictions that create procedural delays in formalizing a claims advocate relationship. In a process where the insurer is already moving quickly, any mechanism that slows a policyholder’s ability to retain professional help tilts the playing field further toward the carrier.

Time is not neutral in a claim. Delays in documentation, early recorded statements made without professional guidance, and premature settlement agreements are among the most common and most costly mistakes policyholders make. Anything that postpones professional engagement increases the likelihood of exactly these errors.

5. A Moratorium on New Public Adjuster Licenses — Freezing the Field

Perhaps the most far-reaching provision of HB 568 is one that receives the least attention: the law institutes a formal moratorium on the issuance of new public adjuster licenses in Kentucky.

This means that no new claims advocates can become licensed to practice in the state for the duration of the moratorium. Existing licensees can continue operating — but the field cannot grow. No new entrants. No additional capacity. A hard ceiling on the number of professionals available to represent Kentucky policyholders.

The practical consequences compound over time. As licensed practitioners retire, relocate, or leave the profession, the pool of available claims advocates in Kentucky shrinks — with no mechanism to replenish it. In a state that regularly faces severe weather events, flooding, and tornado activity, a contracting advocate workforce means longer waits, reduced competition, and ultimately less leverage for policyholders at the negotiating table.

A moratorium on new licenses is not consumer protection. It is supply suppression — and Kentucky homeowners will feel it most acutely after the next major disaster, when demand for professional representation peaks and the licensed professionals available to provide it are fewer than ever.

What Does This Mean For You?

For Kentucky Homeowners and Property Owners

If you experience a significant property loss — fire, flooding, storm damage, or any event that triggers a substantial insurance claim — you have the right to hire a public adjuster to represent you. HB 568 does not eliminate that right. What it does is narrow the window in which your claims advocate can make contact following a disaster, and it may affect the pool of experienced professionals available to take your case.

Know your rights before you need them. If a loss occurs, move as quickly as permitted to engage a licensed claims advocate. Don’t assume the insurer’s adjuster is representing your interests — they are not.

For Policyholders With Underpaid or Disputed Claims

HB 568 applies most acutely to new engagements following a disaster declaration. If you have an existing dispute — an underpaid claim, a denial you believe is incorrect, a settlement offer that doesn’t cover your actual losses — consult a licensed public adjuster now. The law’s restrictions on initial contact do not prevent ongoing representation in active disputes.

For Public Adjusters and Claims Advocates

The legal challenge to HB 568 is active and ongoing. The outcome will shape the regulatory landscape not just in Kentucky but potentially across other states watching the case closely. Practitioners should stay current on the litigation, document any instances where the law’s restrictions demonstrably harm clients, and participate in any public comment or legislative engagement opportunities as they arise.

Frequently Asked Questions

What is a public adjuster?

A public adjuster is a state-licensed professional who represents policyholders — not insurers — in the preparation, presentation, and negotiation of property insurance claims. They are paid on a contingency basis, meaning they receive a percentage of the claim settlement only if they recover money for the client.

What is the difference between a public adjuster and an insurance adjuster?

An insurance adjuster (staff or independent) is hired by and works for the insurance company. A public adjuster — or claims advocate — is hired by and works exclusively for the policyholder. Both use the word “adjuster,” which is a persistent source of confusion that leaves many homeowners believing they’re represented when they’re not.

Is it worth hiring a public adjuster?

For significant property losses, yes. Forbes Advisor’s guide to public adjusters notes that represented policyholders consistently recover higher settlements on average. The contingency fee structure means you typically pay nothing unless your advocate recovers money for you. ¹

What does Kentucky HB 568 do?

HB 568 restricts public adjusters operating in Kentucky through disaster-related solicitation blackouts, contingency fee caps, new licensing requirements, and contract cooling-off periods. The law is subject to an active legal challenge. ²

Why is HB 568 being challenged in court?

Opponents argue it unconstitutionally restricts the rights of licensed professionals and effectively tilts the insurance claims process in favor of carriers at the expense of policyholders. A formal legal challenge was filed ahead of a legislative hearing on the bill. ³

Can new public adjusters get licensed in Kentucky under HB 568?

No. HB 568 includes a formal moratorium on new public adjuster licenses in the state, preventing any new claims advocates from entering the Kentucky market for the duration of the moratorium. This effectively caps the number of licensed professionals available to represent policyholders, with no mechanism to replace those who leave the profession.

How do I find a reputable claims advocate?

Look for state licensure, membership in professional organizations such as the National Association of Public Insurance Adjusters (NAPIA), verifiable references, and full transparency about fee structure before signing any contract. A reputable claims advocate will never pressure you into signing anything immediately.

Can a claims advocate help with a denied claim?

Yes. Reviewing denials, identifying grounds for appeal, and negotiating with the insurer on disputed or rejected claims is core to what public adjusters do.

This content is for informational purposes only and does not constitute legal or insurance advice. For questions about a specific claim, consult a licensed public adjuster or attorney.

Sources

- Forbes Advisor — What Is a Public Adjuster?

- LEX 18 News — Kentucky HB 568: Restricting Public Adjusters Draws Legal Challenge Ahead of Monday Hearing

LEX 18 News — Kentucky HB 568: Legal Challenge