Texas Is Changing the Rules on Insurance Appraisal — Here’s What Every Property Owner Needs to Know

March 12, 2026

Written by Taylor Bezek

Share

The Texas Department of Insurance has proposed sweeping new regulations that will fundamentally reshape how disputed insurance claims get resolved. If your home or auto claim is underpaid, these changes give you clearer, faster tools to fight back — but only if you know how to use them.

Key Takeaways

- What it is: Texas SB 458 mandates that all personal auto and residential property insurance policies include a binding appraisal clause, giving policyholders the unilateral right to dispute underpaid claims

- When it applies: Policies issued, delivered, or renewed on or after January 1, 2026

- Act effective date: September 1, 2025

- TDI rulemaking: Formal proposed rules released April 29, 2026 under Docket 2862 (28 TAC §§5.9800–5.9806)

- Public hearing: June 2, 2026 — comments accepted through June 8, 2026

Who it covers: Residential property and personal auto policyholders — excludes commercial and TWIA policies

What Is Insurance Appraisal in Texas?

Insurance appraisal is a dispute resolution process built into most property owners and auto insurance policies. When you and your insurer disagree on how much your loss is worth, appraisal lets you bring in independent experts — rather than going straight to a lawsuit — to determine a binding dollar amount.

Think of it as an alternative to litigation: each side hires their own appraiser, and if those two can’t agree, a neutral third party called an umpire makes the call. The result is binding.

Despite being one of the most powerful tools available to policyholders, appraisal is used in only a small percentage of Texas claims — largely because most property owners don’t even know it exists.

The Texas Department of Insurance (TDI) is changing that.

What Are the New TDI Appraisal Rules?

TDI has proposed new regulations under 28 TAC §§5.9800–5.9806, implementing Senate Bill 458 (89th Legislature, 2025) and the new Insurance Code Chapter 1813. These rules apply to residential property and personal auto policies issued, delivered, or renewed on or after January 1, 2026. 1

Note: These rules do not apply to commercial property insurance or Texas Windstorm Insurance Association (TWIA) policies.

TDI released its formal proposed rules on April 29, 2026 under Docket 2862 and is currently in the public comment period. 2 3

The proposal transforms appraisal from a loosely-worded contractual clause — which carriers could game with procedural objections — into a standardized, enforceable framework.

The 5 Biggest Changes Under the Proposed Rules

1. You Can Demand Appraisal Unilaterally — No More “Impasse” Games

Under current practice, some insurers argued that appraisal wasn’t available until both parties were at a complete standstill. This “impasse” requirement gave carriers a procedural weapon to delay or block appraisal altogether.

The proposed rules kill that argument. Every covered policy must:

- State that either party can unilaterally demand appraisal

- Prohibit making an “impasse” a condition of access

- Require only that the amount of loss is in dispute

This is a meaningful power shift. Policyholders and their advocates gain clearer leverage to move stalled claims into a defined resolution track — without first fighting over whether they’re even allowed to be there.

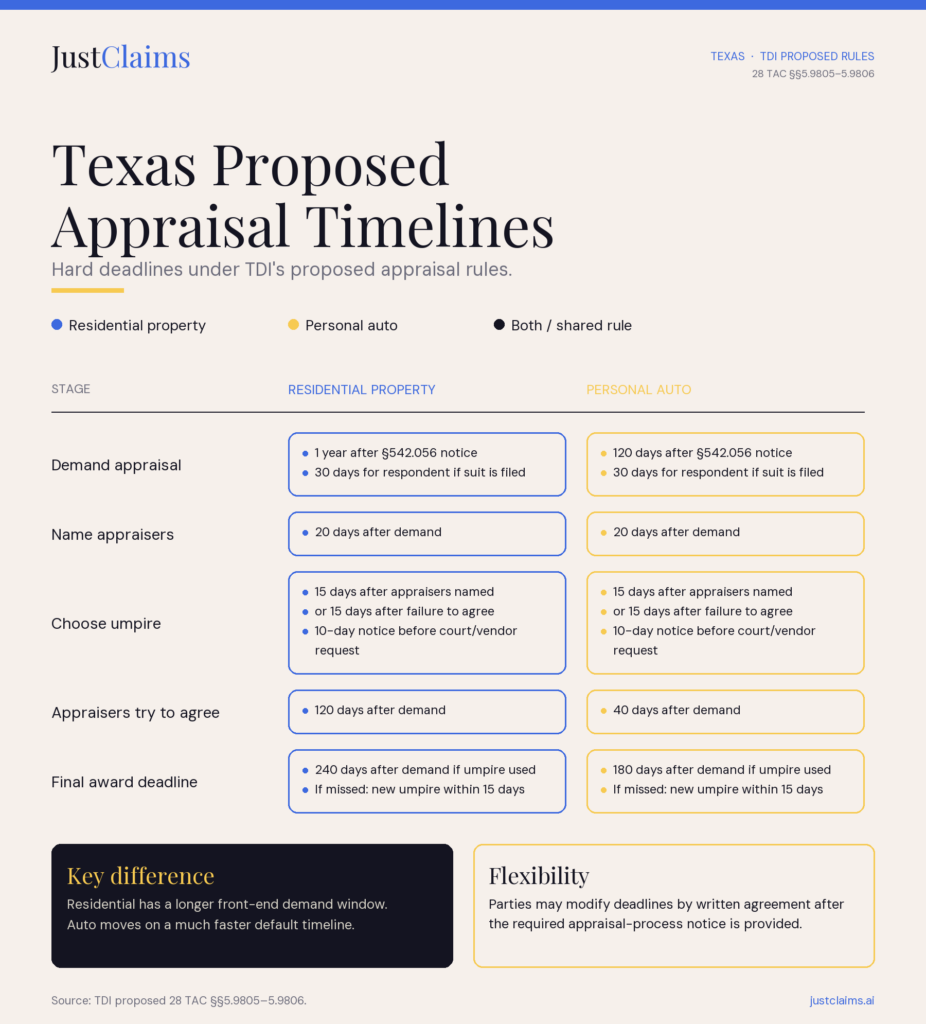

2. Hard, Enforceable Deadlines Replace Vague Timing

This is where the rules get most specific — and most useful. TDI is replacing informal timing norms with locked-in deadlines keyed to your insurer’s claim acceptance or rejection notice under Insurance Code §542.056.

Residential Property Insurance Timelines

| Stage | Deadline |

| Demand appraisal | Within 1 year of §542.056 notice |

| Demand if lawsuit filed | 30 days from filing |

| Each party names appraiser | Within 20 days of demand |

| Appraisers try to agree | Within 120 days of demand |

| Final award (if umpire involved) | Within 240 days of demand |

| Replace umpire if deadline missed | Within 15 days of expiration |

Personal Auto Insurance Timelines

| Stage | Deadline |

| Demand appraisal | Within 120 days of §542.056 notice |

| Demand if lawsuit filed | 30 days from filing |

| Each party names appraiser | Within 20 days of demand |

| Appraisers try to agree | Within 40 days of demand |

| Final award (if umpire involved) | Within 180 days of demand |

| Replace umpire if deadline missed | Within 15 days of expiration |

These timelines can be modified by written agreement between the parties after the appraisal process notice has been provided — but the default framework is now visible, consistent, and enforceable.

3. Appraisers and Umpires Must Meet Minimum Qualifications

For the first time in Texas, the rules codify who is actually qualified to serve as an appraiser or umpire.

All appraisers and umpires must be:

- Competent by training or experience to evaluate the type of loss

- Independent from both parties

- Disinterested in the outcome (no financial stake in the result)

For residential dwelling losses, the bar is higher. Appraisers and umpires must also be one of the following:

- A licensed adjuster or public adjuster with residential loss estimating experience

- An engineer or architect with residential construction or damage investigation experience

- Someone with direct occupational experience constructing, repairing, or estimating the type of property at issue

This matters because unqualified appraisers skew awards — and have historically been used as a strategy by well-resourced carriers to neutralize the process. These rules raise the floor for everyone.

4. Insurers Must Proactively Tell You Appraisal Exists

TDI’s own data shows that appraisal is used in only a small fraction of claims, and is almost always initiated by the policyholder. The likely reason? Most property owners and auto policyholders have never heard of it.

Under the proposed rules, every time an insurer sends you a claim acceptance or rejection notice, they must also send a plain-language appraisal process notice that explains:

- Where the appraisal clause is in your policy

- How to make a demand, including where to send it

- Your responsibilities and potential costs

- How to get an umpire appointed (including through a court)

- All applicable deadlines

- What a binding appraisal award means for your claim

This is a significant consumer protection step — and it means carriers can no longer rely on policyholders simply not knowing they have options.

5. Umpire Selection Gets Clearer Rules (With a Fallback)

When appraisers can’t agree on who the umpire should be, the rules now standardize what happens. Policies must:

- Allow either party to request judicial appointment of an umpire through a county or district court where the property is located

- Require 10 days’ written notice before filing any umpire appointment request

- Give the other party a copy of the request before or when it’s submitted

Insurers can also include vendor-based umpire selection, but only if the policyholder gets to choose the vendor from at least two options, or if only the policyholder can invoke that method. The judicial fallback cannot be removed.

What Does This Mean If Your Claim Has Been Underpaid?

For Property Owners

If your insurer’s offer won’t cover your actual repair costs, you now have a clearer path to challenge it. The one-year demand window gives you time to document the gap, hire the right appraiser, and push for a fair outcome — without having to argue about whether you’re even entitled to appraisal.

For Auto Policyholders

The 120-day demand window is shorter, so if you believe your total loss or repair valuation is off, move quickly once you receive your insurer’s §542.056 notice.

For Public Adjusters and Contractors

These rules create cleaner timelines for appraisal engagements and raise the floor on appraiser qualifications 4 — which benefits legitimate professionals in the space. The removal of the impasse requirement also opens appraisal earlier in the dispute cycle, before positions harden.

Frequently Asked Questions

When do these rules take effect?

SB 458 was signed into law on June 20, 2025, and took effect September 1, 2025 for new policies. The mandatory appraisal provisions apply to all policies issued, delivered, or renewed on or after January 1, 2026 5 6. TDI released its formal proposed implementing rules on April 29, 2026 under Docket 2862 and is currently accepting public comments. 7

Do these rules apply to my commercial property policy?

No. These rules apply only to residential property and personal auto insurance. Commercial property policies are excluded.

What if my insurer refuses to go to appraisal?

Under the proposed rules, either party can unilaterally demand appraisal — no insurer consent required. If an insurer improperly refuses, that refusal may itself create legal exposure. 8

Can deadlines be extended?

Yes — but only by written agreement between both parties, and only after the insurer provides the mandatory appraisal process notice.

Do I need a public adjuster for appraisal?

You’re not required to hire one, but the process is technical, deadline-driven, and carries binding consequences. Having a licensed public adjuster with residential estimating experience — now required under the proposed qualification rules — on your side materially affects the outcome.

What is a “disinterested” appraiser?

The legal term “disinterested” means the appraiser has no financial stake in the outcome. They’re not paid a percentage of the award, and they don’t have a business relationship that would bias their valuation.

The Bottom Line

Texas appraisal law has long favored those with the most resources, the most knowledge, and the most procedural leverage. These proposed TDI rules begin to level that playing field — by mandating clear timelines, forcing carriers to inform policyholders of their rights, eliminating the impasse trap, and setting a floor on who can actually serve as an appraiser. 9 10

For property owners who’ve been told an inadequate settlement is “the best we can do,” these rules create new, enforceable tools to demand otherwise.

The clock starts when your insurer sends its acceptance or rejection notice. Know your rights before it starts.

This content is for informational purposes only and does not constitute legal or insurance advice. For questions about a specific claim, consult a licensed public adjuster or attorney.

Sources

- Texas Department of Insurance — TDI Proposed Rule 28 TAC §§5.9800–5.9806 (Informal Draft)

tdi.texas.gov/rules/2025/documents/59800informal.pdf ↩︎ - LegiScan — SB 458 Full Bill Text, 89th Legislature

legiscan.com/TX/text/SB458/id/3245674

↩︎ - Property Insurance Coverage Law Blog — Texas SB 458: What Homeowners and Drivers Need to Know

propertyinsurancecoveragelaw.com/blog/texas-sb-458 ↩︎ - Property Insurance Coverage Law Blog — Texas SB 458: Appraiser Qualifications

propertyinsurancecoveragelaw.com/blog/texas-sb-458 ↩︎ - Texas Department of Insurance — TDI Proposed Rule 28 TAC §§5.9800–5.9806 (Informal Draft)

tdi.texas.gov/rules/2025/documents/59800informal.pdf ↩︎ - Texas Department of Insurance — TDI Rulemaking Web Cover, 59800

tdi.texas.gov/rules/2025/documents/59800webcover.pdf ↩︎ - LegiScan — SB 458 Full Bill Text, 89th Legislature

legiscan.com/TX/text/SB458/id/3245674 ↩︎ - Property Insurance Coverage Law Blog — Texas SB 458: Insurer Refusal to Appraise

propertyinsurancecoveragelaw.com/blog/texas-sb-458 ↩︎ - LegiScan — SB 458 Full Bill Text, 89th Legislature

legiscan.com/TX/text/SB458/id/3245674 ↩︎ - Property Insurance Coverage Law Blog — Texas SB 458: Overview

propertyinsurancecoveragelaw.com/blog/texas-sb-458 ↩︎

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. After founding his own firm, Taylor saw firsthand the institutional asymmetry property owners face and joined JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor’s mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.