Your Property Just Got Hit by Hail. Here’s What to Do Before You File Anything.

June 03, 2026

Written by Taylor Bezek

Share

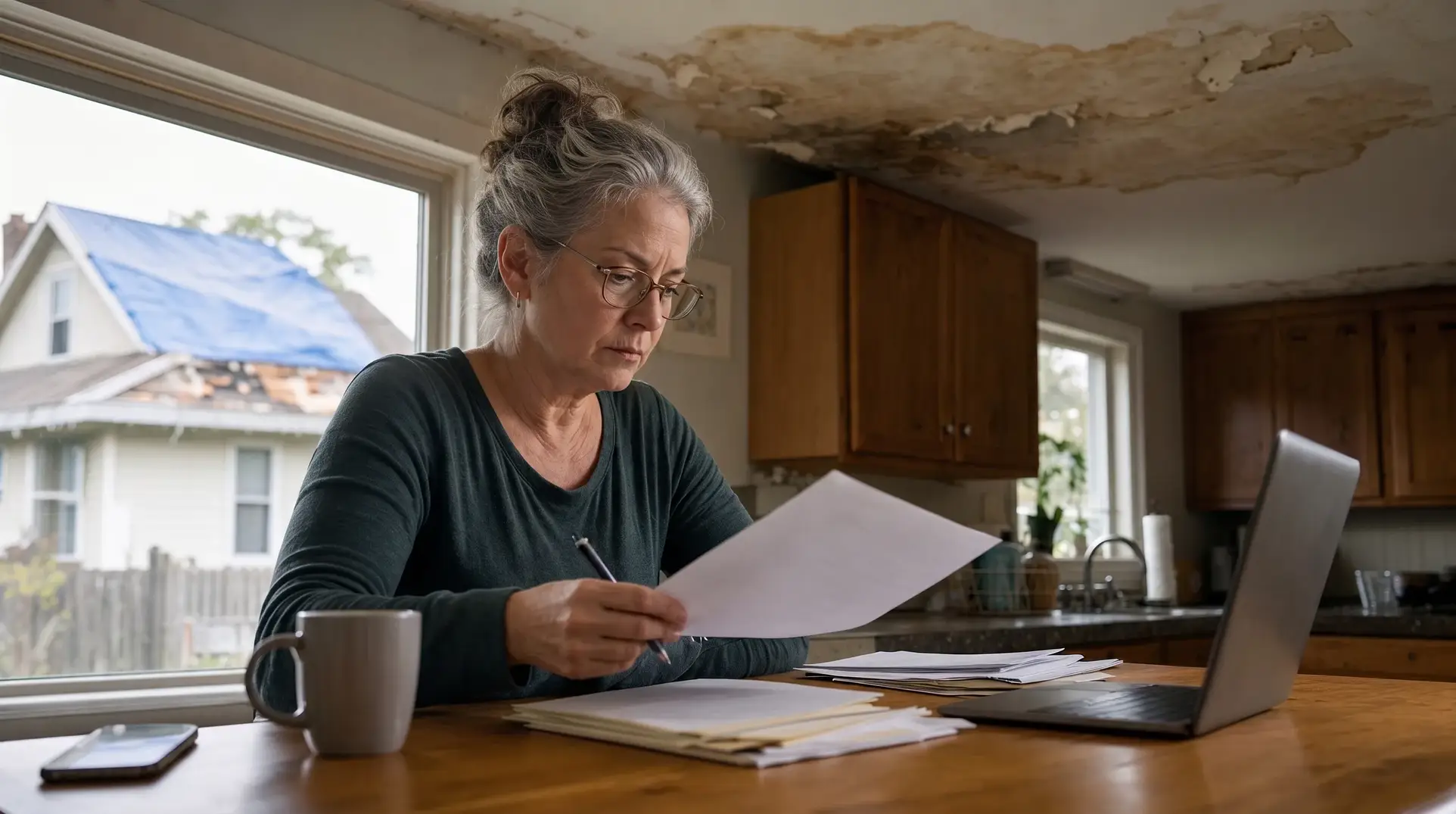

Monday’s storm wasn’t subtle. Golf ball-sized hail moved across the Denver metro, and if you own commercial property in the area — a retail center, an office building, a warehouse, an HOA community — there’s a good chance you have damage you haven’t fully assessed yet.

That’s normal. What matters now is what you do next.

Because the single most expensive mistake property owners make after a hail event isn’t filing too late. It’s filing too early, without understanding what damage they actually have.

The Instinct to Ignore It Is Understandable — and Costly

A lot of commercial property owners see hail damage and think one of two things: either it looks minor so it probably is, or the insurance company will figure it out. Both assumptions quietly cost money.

Hail damage on commercial roofs, HVAC equipment, skylights, siding, and other envelope components is frequently more extensive than a surface-level look reveals. And insurance carriers, whatever their intent, issue initial estimates based on what their adjuster documents — not what’s actually there. If your property isn’t fully assessed before that estimate goes out, the gap between what you’re owed and what you’re offered can be significant.

Denver County alone averages $279 million in projected annual hail damage per year, with 9 to 10 significant hail events annually. The 2024 metro hailstorm caused nearly $2 billion in damage across Colorado. This is not a market where hail claims are rare or simple.

What Insurers Look at — and What They Often Miss

When a carrier sends an adjuster after a storm, the goal is to document the visible loss and issue a reserve. What that process frequently misses:

Code and ordinance requirements. Commercial roof replacements often trigger current code requirements that weren’t part of the original installation — drainage upgrades, membrane specifications, parapet details, insulation R-value minimums. These are legitimate covered costs under most policies, and they’re routinely omitted from first estimates.

Hidden and consequential damage. What’s visible from a rooftop walk-through is not the full picture. Damaged decking, compromised insulation, interior moisture infiltration that hasn’t surfaced yet — these items may only become apparent once work begins. By then, you’re mid-project and fighting for a supplement.

Mechanical and envelope damage. HVAC units, skylights, gutters, downspouts, signage, and exterior lighting are all hail-vulnerable and commonly under-documented in commercial claims.

Business interruption and soft costs. Depending on your policy and the nature of the loss, you may have coverage for more than just the physical damage — temporary repairs, engineering, relocation costs, and lost income during restoration may all be in play.

Debris removal coverage is another line item owners routinely overlook — hauling away a destroyed commercial roof, fallen signage, or ruined interior finishes carries real cost and is usually capped by its own sub-limit that carriers rarely highlight.

Matching and uniformity. On commercial properties, partial repairs that don’t match existing systems or finishes can create ongoing liability exposure, warranty gaps, and tenant disputes. Carriers often propose patches when full-system replacement is the appropriate remedy.

Colorado Law Is On Your Side — If You Know How to Use It

Colorado gives commercial property owners real legal leverage that most never use.

Appraisal. When a claim is disputed or undervalued, Colorado allows policyholders to invoke an appraisal process that resolves amount-of-loss disputes — including causation questions like whether specific damage was caused by this storm versus pre-existing wear. This is a binding, policy-based process that doesn’t require full litigation and can often resolve disputes far more efficiently.

Unreasonable delay protections. Colorado law prohibits insurers from unreasonably delaying or denying covered benefits. When that happens, a policyholder may be entitled to two times the covered benefit that was unreasonably delayed or denied, plus attorney fees and court costs. Carriers know this, and it changes how they respond when claims are properly managed.

The Mistake That’s Easy to Make Right Now

The most common misstep we see commercial property owners make in the days after a storm: they call their carrier, report the loss, and wait for the adjuster — without doing any independent documentation first.

That sequence hands the carrier complete control over how the claim is framed. The adjuster’s scope becomes the default. Everything you add later is a supplement. Every supplement requires documentation, follow-up, and negotiation.

The owners who end up in the best position are the ones who understand what they have before anyone else does.

What to Actually Do This Week

You don’t need to be a claims expert. You need to ask the right questions before the adjuster shows up.

Get an independent assessment of the damage. Don’t rely solely on the carrier’s adjuster to tell you what you have. A qualified inspection before the first estimate is issued gives you a basis to compare against — and documentation to support your position if disputes arise.

Review your policy before you file. Know what coverages you have — replacement cost vs. actual cash value, ordinance and law coverage, equipment breakdown, business interruption. “It is also worth checking your policy’s insurance to value requirement, because an understated building limit can trigger a coinsurance penalty that reduces every dollar the carrier pays on a hail loss. Most owners don’t read their policy until a claim is already in dispute.

Don’t accept the first estimate as final. Initial estimates on commercial hail claims are routinely incomplete. That doesn’t mean the carrier is acting in bad faith — it means the process is imperfect and advocacy matters.

Bring in help early. A public adjuster works for you, not the carrier. Their job is to make sure the claim reflects the actual loss — including everything that’s easy to miss, overlook, or delay. Engaging one before the claim is filed or before the first estimate is issued puts you in a fundamentally stronger position than engaging one after you’ve already hit a wall.

The Bottom Line

Hail claims on commercial property are not simple. The damage is often more extensive than it appears, the coverage is often more comprehensive than owners realize, and the process rewards the parties who are best prepared.

If you own commercial property in the Denver metro and want to understand what you actually have before making decisions, we’re offering free claim reviews for property owners affected by this week’s storm.

No commitment. No pressure. Just a clear picture of your damage, your coverage, and your options — before you file anything.

→ Contact us at partner@justclaims.ai or learn more here.

JustClaims is a licensed Public Adjuster serving commercial and residential property owners across Colorado. We handle hail, wind, fire, and water claims — and we exist so you don’t have to navigate the process alone.

Sources

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. A licensed Public Adjuster in TX (#2125659), FL (#W455048), CO (#769172), and 10 additional states, Taylor founded his own firm before joining JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor's mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.