Commercial Hail Damage Insurance Claims: 2026 Guide

June 01, 2026

Written by Taylor Bezek

Share

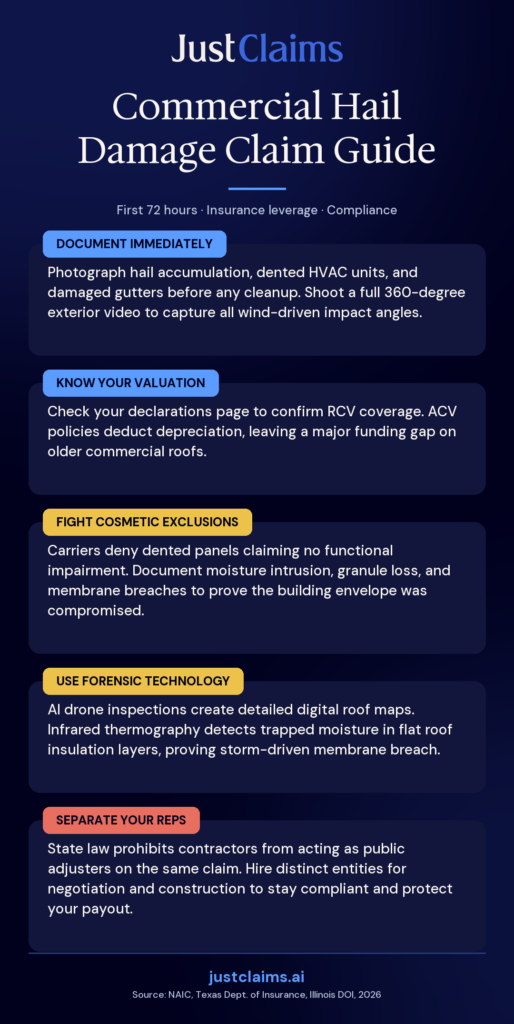

Commercial hail damage requires precise, immediate documentation to prevent insurers from minimizing large-scale repair costs. Property owners and contractors must capture comprehensive evidence, including full 360-degree exterior videos, to substantiate complex losses. Understanding policy nuances and leveraging advanced diagnostic tools ensures that legitimate claims are accurately valued and paid.

Key Takeaways

- Visual Evidence: Document hail size by photographing hailstones next to a ruler or coin for scale, and capture video from all exterior elevations to record directional impact patterns [10].

- Safety Protocol: Maintenance personnel should avoid walking on the roof without proper training, as it can worsen damage or create safety risks.

- Coverage Types: Replacement Cost Value (RCV) coverage pays the full cost to repair or replace damaged property with materials of similar kind and quality, without deducting for depreciation.

- Fee Limits: Public adjusters typically charge a fee based on a percentage of the total claim settlement, which in states like Texas is capped at 10% of the total amount paid by the insurance company.

- Contract Rules: State regulations often provide a cancellation window for public adjuster contracts; for example, Illinois allows policyholders to cancel the contract within five business days of signing.

Immediate Post-Storm Steps for Commercial Properties

When a hailstorm strikes a commercial building, the initial response sets the foundation for the entire insurance claim. Property managers should immediately document the storm’s impact by taking photos of hail accumulation on the ground, dented metal surfaces, and damage to rooftop equipment or screens [1]. This immediate action preserves perishable evidence before the ice melts or cleanup crews alter the scene.

1. Ground-Level Visual Documentation

Before attempting any elevated inspections, a ground-level inspection can reveal indicators of roof damage, such as dented HVAC housings, damaged gutters, or pieces of roofing material on the ground [1]. Documenting these early signs establishes a clear timeline of the storm’s immediate physical impact. Contractors can assist by walking the perimeter with property managers to identify collateral damage to siding, windows, and exterior lighting, which often correlates with the severity of the impacts on the roof membrane above.

2. Exterior Video and Scale Measurements

Photographic evidence must provide context to be useful during the adjustment process. Documenting hail size using a ruler or coin for scale, and recording video from all exterior elevations, helps establish the storm’s directionality and the scope of impacts. This comprehensive visual record prevents disputes over the extent of damage and provides a baseline for the formal roof inspection that follows [10].

3. Roof Access and Safety Protocols

While it is tempting to immediately assess the roof membrane, maintenance personnel should avoid walking on the roof without proper training, as it can worsen damage or create safety risks; instead, a professional roof inspection should be scheduled [1]. Commercial roofs often feature complex geometries, skylights, and weakened decking after a severe weather event. Relying on specialized contractors ensures that the initial assessment complies with safety regulations and prevents inadvertent spoliation of evidence.

Navigating Commercial Policy Valuations and Exclusions

Because initial documentation only goes so far, understanding how the commercial policy values that documented damage is the next critical step in the recovery process. The specific language in the insurance contract dictates whether a property owner receives enough funds to complete necessary repairs or is left with a massive deficit.

1. Replacement Cost Value (RCV)

Replacement Cost Value (RCV) coverage pays the full cost to repair or replace damaged property with materials of similar kind and quality, without deducting for depreciation [3]. For contractors and builders, ensuring the claim is processed under RCV is vital to covering the actual market rates for labor and commercial-grade materials. Property owners must verify their declarations page to confirm RCV applies to the roof system, as some policies may default older roofs to a different valuation method. Large hail losses also generate significant cleanup costs, so owners should confirm their debris removal coverage, which typically pays to haul away destroyed roofing and equipment up to a separate sub-limit tied to the direct damage payment.

2. Actual Cash Value (ACV)

In contrast, Actual Cash Value (ACV) coverage pays the depreciated cost to repair or replace damaged property, factoring in the property’s age and remaining useful life [4]. If a commercial policy defaults to ACV, the resulting payout may leave a significant financial gap, requiring the property owner to fund the difference out of pocket. Contractors must be prepared to explain depreciation schedules to their clients, as an ACV settlement on an older commercial roof will yield a fraction of the funds required for a full replacement.

3. Cosmetic Damage Exclusions

Insurers often include ‘roof surfacing’ or cosmetic damage exclusions to limit coverage for superficial hail damage that alters a roof’s appearance but does not impair its function as a moisture barrier [4]. Contractors must carefully review the policy language to determine if these exclusions apply, as adjusters frequently cite them to deny claims for dented metal panels or HVAC casings that are still technically operational. Owners should also review any protective safeguards endorsement on the commercial policy, since it conditions coverage on maintaining specified protective systems and can give the carrier grounds to reduce a payout if those systems are not kept in service.

Advanced Evidence Gathering and Forensic Engineering

When policy exclusions threaten to minimize the payout, advanced diagnostic evidence becomes the primary defense against underpayment. Modern commercial claims increasingly rely on technological assessments to prove that hail impacts compromised the building envelope, moving the conversation from subjective opinions to objective data.

1. AI-Powered Drone Inspections

Drones equipped with AI technology can automatically detect subtle hail damage, such as dislodged granules, and capture hundreds of aerial images to create highly detailed digital roof reproductions [5]. According to drone inspection providers, AI-based damage detection reduces the amount of manual inspection work and helps standardize how damage is identified, which can make it more difficult for insurance companies to dismiss well‑documented, AI‑supported reports. [5]. Property owners can leverage these digital twins to track the exact location and density of hail hits across massive commercial complexes, ensuring no damaged section is overlooked by the field adjuster.

2. Advanced Diagnostic Scanning

Forensic engineers utilize drones to safely inspect difficult-to-access roof areas, reducing the need for expensive lifts or scaffolding while providing accurate photographic and video documentation. Beyond standard photography, advanced diagnostic tools used by forensic engineers, including drone inspections, 3D scanning, and infrared thermography, help validate event-driven losses and identify the true origin of roof damage [7]. Infrared thermography is particularly crucial for flat commercial roofs, as it detects trapped moisture within the insulation layer, proving that the waterproof membrane was breached during the storm.

3. Comprehensive Engineering Reports

A comprehensive forensic engineering report strengthens claim defensibility by providing evidence-backed causation, clear timelines tied to specific storm events, and repair recommendations aligned with engineering standards [7]. For contractors managing large-scale commercial repairs, these reports provide the technical authority needed to counter an adjuster’s assertion of pre-existing wear and tear. When an insurer attempts to attribute roof leaks to poor maintenance, an engineering report detailing the exact physics of the hail impact serves as the definitive rebuttal.

Professional Support and Regulatory Guidelines

Even with forensic evidence in hand, navigating the final settlement often requires specialized professional support bound by strict state regulations. Large commercial losses frequently involve third-party advocates to manage the complex negotiation process and ensure compliance with local insurance codes.

1. The Role of Public Adjusters

Public adjusters work exclusively on behalf of the policyholder to assist in the preparation, presentation, and settlement of an insurance claim, rather than representing the insurance company [8]. They handle the administrative burden of the claim, allowing property owners and builders to focus on mitigating further loss and planning the reconstruction. By interpreting complex policy language and compiling detailed loss estimates, public adjusters level the playing field against the carrier’s internal adjustment team.

2. Contractor and Adjuster Separation Laws

State laws strictly regulate who can advocate for the policyholder and who can perform the repairs. In Texas, public adjusters are legally prohibited from acting as the contractor for the same claim, and contractors are similarly barred from advertising that they will handle the insurance claim [9]. This separation ensures a conflict-free assessment of the damage. Property owners must hire distinct entities for the negotiation phase and the construction phase to remain compliant with state statutes and avoid voiding their claim.

3. Fee Caps and Cancellation Windows

When hiring representation, property owners must understand the financial and contractual terms. Public adjusters typically charge a fee based on a percentage of the total claim settlement, which in states like Texas is capped at 10% of the total amount paid by the insurance company [9]. Additionally, state regulations often provide a cancellation window for public adjuster contracts; for example, Illinois allows policyholders to cancel the contract within five business days of signing [8]. Reviewing these contractual safeguards ensures that commercial entities maintain control over their financial recovery strategy.

Frequently Asked Questions

What is the difference between RCV and ACV in commercial hail claims?

Replacement Cost Value (RCV) covers the full expense of repairing or replacing damaged property with materials of similar quality, without factoring in depreciation [3]. Actual Cash Value (ACV) only pays the depreciated cost, which accounts for the age and remaining useful life of the roof or equipment [4]. Understanding this distinction is critical for contractors estimating out-of-pocket costs for property owners.

How can drones improve a commercial roof inspection?

Drones equipped with AI technology can automatically detect subtle hail damage and capture hundreds of aerial images to create detailed digital roof reproductions [5]. Forensic engineers also utilize drones to safely inspect difficult-to-access roof areas, reducing the need for expensive lifts or scaffolding while providing accurate documentation [6].

Can a roofing contractor also act as my public adjuster?

In many jurisdictions, strict laws prevent this conflict of interest. For example, in Texas, public adjusters are legally prohibited from acting as the contractor for the same claim, and contractors are similarly barred from advertising that they will handle the insurance claim [9]. Property owners must hire separate entities for claim negotiation and physical repairs.

What are cosmetic damage exclusions?

Insurers often include ‘roof surfacing’ or cosmetic damage exclusions to limit coverage for superficial hail damage [4]. This means if a hailstorm alters a roof’s appearance but does not impair its function as a moisture barrier, the insurance company may deny the repair costs [4]. Contractors must document functional impairment to overcome these specific policy exclusions.

How to Protect Your Scope and Reputation

Securing a fair payout for commercial hail damage requires meticulous documentation, a deep understanding of policy valuations, and the right technical evidence. By leveraging forensic engineering and adhering to state regulations regarding professional representation, contractors and property owners can ensure that legitimate damage is properly funded. If your contractor claim was denied, JustClaims‘ AI reviews your policy language and flags underpayments before you dispute.

This content is for informational purposes only and does not constitute legal or insurance advice.

Sources

[2] https://www.vosslawfirm.com/blog/how-to-document-hail-damage-on-a-commercial-property.cfm

[4] https://www.hailsolve.com/blog/hail-risk-management-terms

[5] https://www.eagleview.com/construction/how-drone-inspections-can-help-identify-hidden-roof-damage/

[6] https://usforensic.com/roof-hail-damage-assessments/

[9] https://www.tdi.texas.gov/tips/public-adjusters.html

[10] https://southernloss.com/best-practices-documenting-hailstorm-damage-catastrophic-event/

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. A licensed Public Adjuster in TX (#2125659), FL (#W455048), CO (#769172), and 10 additional states, Taylor founded his own firm before joining JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor's mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.