Ohio Commercial Hail Damage Claims: A Step-by-Step Guide

May 29, 2026

Written by Taylor Bezek

Share

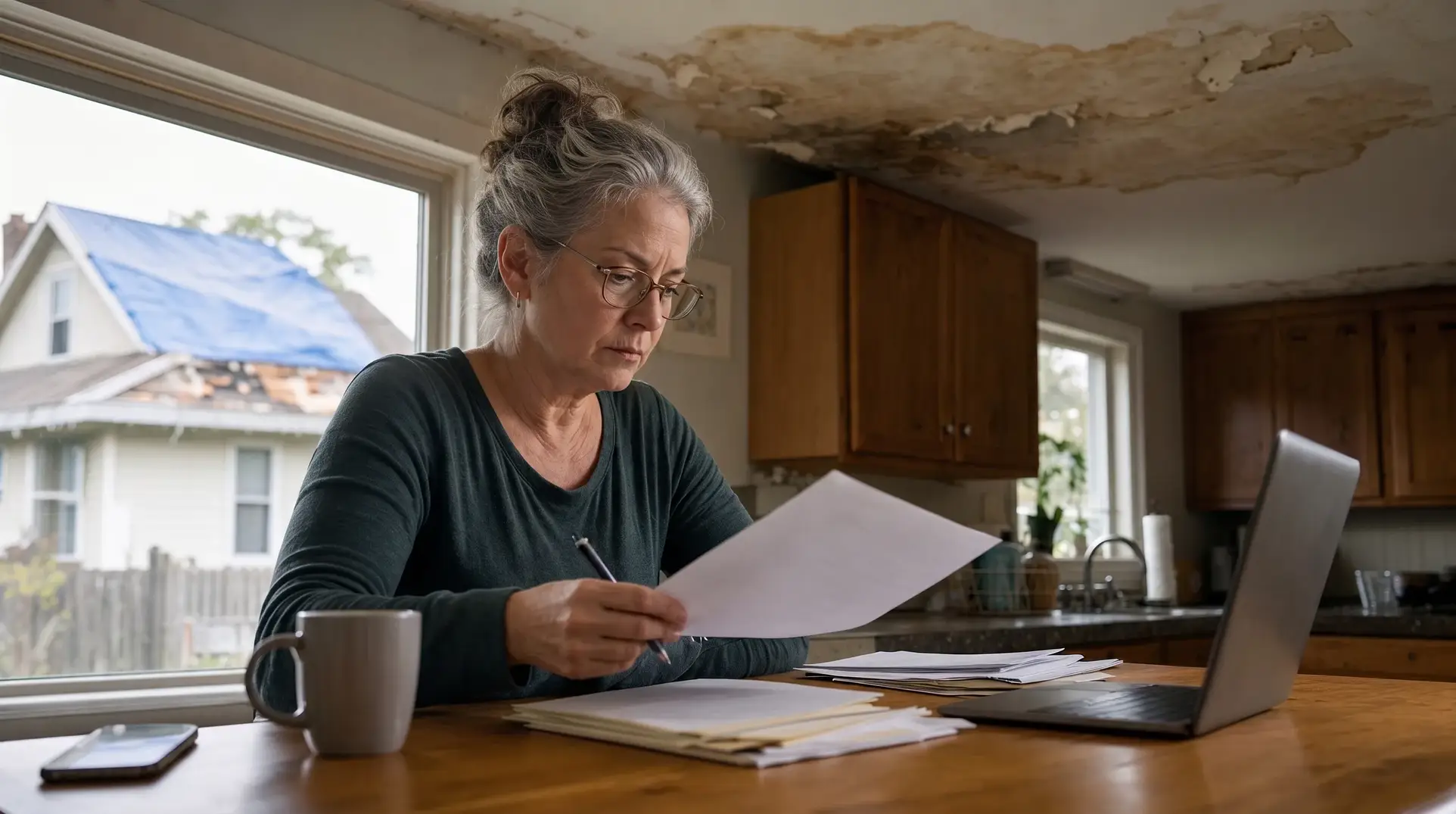

When a severe storm strikes an Ohio business, the first step in a commercial property damage claim is conducting a thorough inspection and taking detailed photographs of all visible impacts. Even small discrepancies in damage valuation can translate to significant losses, making meticulous documentation and a comprehensive inventory of damaged items essential to support your financial recovery.

Key Takeaways

- Initial action: The first step in a commercial property storm damage claim is assessing the damage, which involves conducting a thorough inspection and taking detailed photographs of all visible damage.

- Preparation requirement: Before filing a claim, commercial property owners should review their insurance policy to understand coverage limits, deductibles, and specific provisions related to storm damage.

- Evidence collection: Meticulous documentation is required to support the claim, including creating a comprehensive inventory of damaged items and obtaining multiple repair estimates from licensed contractors.

- Dispute tracking: During the claims process, it is crucial to document all communication with the insurance company, including emails, phone calls, and meetings, to track progress and serve as evidence in disputes.

- Escalation options: If the insurance settlement is insufficient or difficulties arise, commercial property owners can seek assistance from a public adjuster or an attorney specializing in insurance claims to help maximize recovery.

Immediate Steps After a Hail Event

1. Assessing the Damage

The first step in a commercial property storm damage claim is assessing the damage, which involves conducting a thorough inspection and taking detailed photographs of all visible damage [1]. Property owners should capture wide-angle shots of the entire facility alongside close-up images of specific impact points. Documenting the immediate aftermath helps establish a clear baseline of the destruction before any temporary repairs alter the scene.

2. Reviewing Policy Provisions

Before filing a claim, commercial property owners should review their insurance policy to understand coverage limits, deductibles, and specific provisions related to storm damage [1]. Commercial policies often contain complex endorsements, such as cosmetic damage exclusions or specific requirements for Business Interruption coverage. Another endorsement worth checking is the protective safeguards endorsement, which conditions coverage on the owner maintaining specified protective systems and can be used by a carrier to reduce a payout if those systems are not maintained. Understanding these parameters early in the process helps set accurate expectations for the financial recovery effort. Owners should also confirm that the building values listed on their statement of values insurance schedule are current, because an understated value can trigger a coinsurance penalty that shrinks the hail payout

3. Creating a Comprehensive Inventory

Meticulous documentation is required to support the claim, including creating a comprehensive inventory of damaged items and obtaining multiple repair estimates from licensed contractors [1]. This inventory should encompass not only structural components but also damaged equipment, interior finishes, and affected merchandise. Providing a highly detailed list supports the position that the business suffered extensive losses and requires a thorough valuation.

Understanding Ohio Insurance Claim Protections

Knowing your rights and tracking every interaction with your carrier can help protect your business from bad faith practices. During the claims process, it is crucial to document all communication with the insurance company, including emails, phone calls, and meetings, to track progress and serve as evidence in disputes [1].

Hail damage assessments often require expert evaluation well beyond the carrier’s initial inspection, and having a clear paper trail demonstrates that your business acted promptly and transparently. If an adjuster delays a response or provides conflicting information regarding your coverage, your communication log becomes a vital tool. Recording the dates, times, and summaries of every conversation puts the carrier on notice that you are actively monitoring the handling of your file.

Identifying Hidden Damage on Commercial Roof Systems

Commercial roofing materials often hide hail impact damage from untrained eyes, making expert inspection critical to a complete and well-supported claim.

1. Flat Roof Systems (TPO and EPDM)

TPO and EPDM membranes can sustain hail impacts that may not be immediately visible as punctures or cracks on the surface, but may include localized insulation compression or membrane stress that can be confirmed through physical inspection techniques such as core sampling, moisture metering, or infrared scanning. A thorough inspection should look beyond surface-level damage to identify signs such as insulation compression, membrane stress, or seam integrity issues that may not be immediately apparent. Because flat membrane systems rely on a continuous waterproof layer, repeated or significant hail impacts can compromise the membrane over time and may contribute to water intrusion if damage goes undetected and unrepaired.

2. Sloped Commercial Roofs

Sloped structures face different vulnerabilities, particularly around flashing, HVAC vents, and parapet walls. Taking detailed photographs of all visible damage — including roofing, siding, windows, signage, and other exterior and interior elements — helps document the full scope of the loss for the insurance claim. Hail driven by high winds can dent metal panels, crack tiles, or dislodge shingles, compromising the building envelope and exposing the interior to subsequent weather events.

3. Building Code and Ordinance Upgrades

When repairing extensive roof damage, Ohio commercial building codes may require full system upgrades rather than simple patching. Law & Ordinance (or Ordinance or Law) coverage is typically a separate endorsement — standard commercial property policies may include only minimal built-in limits, which are often insufficient for significant rebuilds — that covers the increased costs of rebuilding to current building codes after a covered loss. It has its own sub-limits and three distinct coverage components — Coverage A (loss in value of undamaged portions that must be demolished), Coverage B (cost to demolish those undamaged portions), and Coverage C (increased construction costs to meet current code) — all of which carry their own sub-limits and must be negotiated separately

Navigating the Appraisal Process and Claim Disputes

Even small discrepancies in damage valuation can translate to significant losses, making it essential to escalate a disputed claim through the proper channels to recover your full policy value.

1. Obtaining Independent Estimates

Obtaining multiple repair estimates from licensed contractors can provide independent cost benchmarks that support a policyholder’s position in negotiations over an underpaid claim. Relying solely on the insurance adjuster’s pricing software often results in a valuation gap. Independent bids from local professionals reflect the true market cost of labor and materials required to restore the facility.

2. Engaging a Public Adjuster

If the insurance settlement is insufficient or difficulties arise, commercial property owners can seek assistance from a public adjuster [1]. These licensed professionals work exclusively on behalf of the policyholder, utilizing their expertise to evaluate the loss accurately and negotiate directly with the insurance carrier.

3. Consulting Legal Counsel

When negotiations stall or bad faith tactics are suspected, property owners may consult an attorney specializing in insurance claims. In Ohio, the standard for bad faith established by the Ohio Supreme Court in Zoppo v. Homestead Ins. Co. (1994) requires showing that the insurer’s refusal to pay was not predicated upon circumstances that furnish reasonable justification therefor — a standard that documented communication and a thorough claims file directly supports [2]. Documented communication, including emails and meeting notes, will serve as vital evidence in these legal disputes [1]. Legal intervention can help enforce the terms of the policy and hold the carrier accountable for unfair claims handling practices.

Frequently Asked Questions

What is the first thing I should do after a storm hits my commercial building?

The initial phase of managing a storm loss involves evaluating the physical impacts on your facility. You must perform a detailed visual check and capture high-quality images of any apparent destruction [1].

Why do I need to read my insurance policy before contacting the carrier?

Examining your coverage documents allows you to grasp your financial responsibilities, such as deductibles, and your maximum payout caps. It also clarifies any unique clauses tied to weather-related losses before you formally initiate the process [1].

How should I keep track of my interactions with the insurance adjuster?

Maintaining a strict log of all correspondence, including phone logs, digital messages, and in-person discussions, is highly recommended. This detailed record helps monitor the status of your file and provides necessary proof if a disagreement occurs [1].

What are my options if the insurance company offers an inadequate payout?

When a carrier’s financial offer falls short of your actual repair needs, you have the right to bring in outside experts. Hiring a specialized legal professional or a public adjuster can assist in pursuing a more accurate and comprehensive financial resolution [1].

How to Protect Your Commercial Property Settlement

Securing a fair payout for your Ohio facility requires proactive documentation, a deep understanding of your policy limits, and a willingness to challenge inadequate offers. Because hail damage assessments often require expert evaluation well beyond the carrier’s initial inspection, relying solely on that first report often leaves significant funds on the table. If your insurance claim was denied or underpaid, JustClaims’ expert team — accelerated by our bespoke AI — reviews the policy language, compares it against your documentation, and flags likely underpayments so you can go back to the carrier with confidence.

This content is for informational purposes only and does not constitute legal or insurance advice. Coverage decisions depend on the specific terms, conditions, and exclusions of each policy and the laws of the applicable jurisdiction; policyholders and contractors should consult with a qualified professional for advice on their particular situation.

Sources

[1] https://content.naic.org/sites/default/files/publication-post-disaster-claims-guide.pdf

[2] https://www.supremecourt.ohio.gov/rod/docs/pdf/0/1994/1994-Ohio-461.pdf

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. A licensed Public Adjuster in TX (#2125659), FL (#W455048), CO (#769172), and 10 additional states, Taylor founded his own firm before joining JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor's mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.