Maximize Your Tornado Damage Claim Recovery Results 2026

May 22, 2026

Written by Taylor Bezek

Share

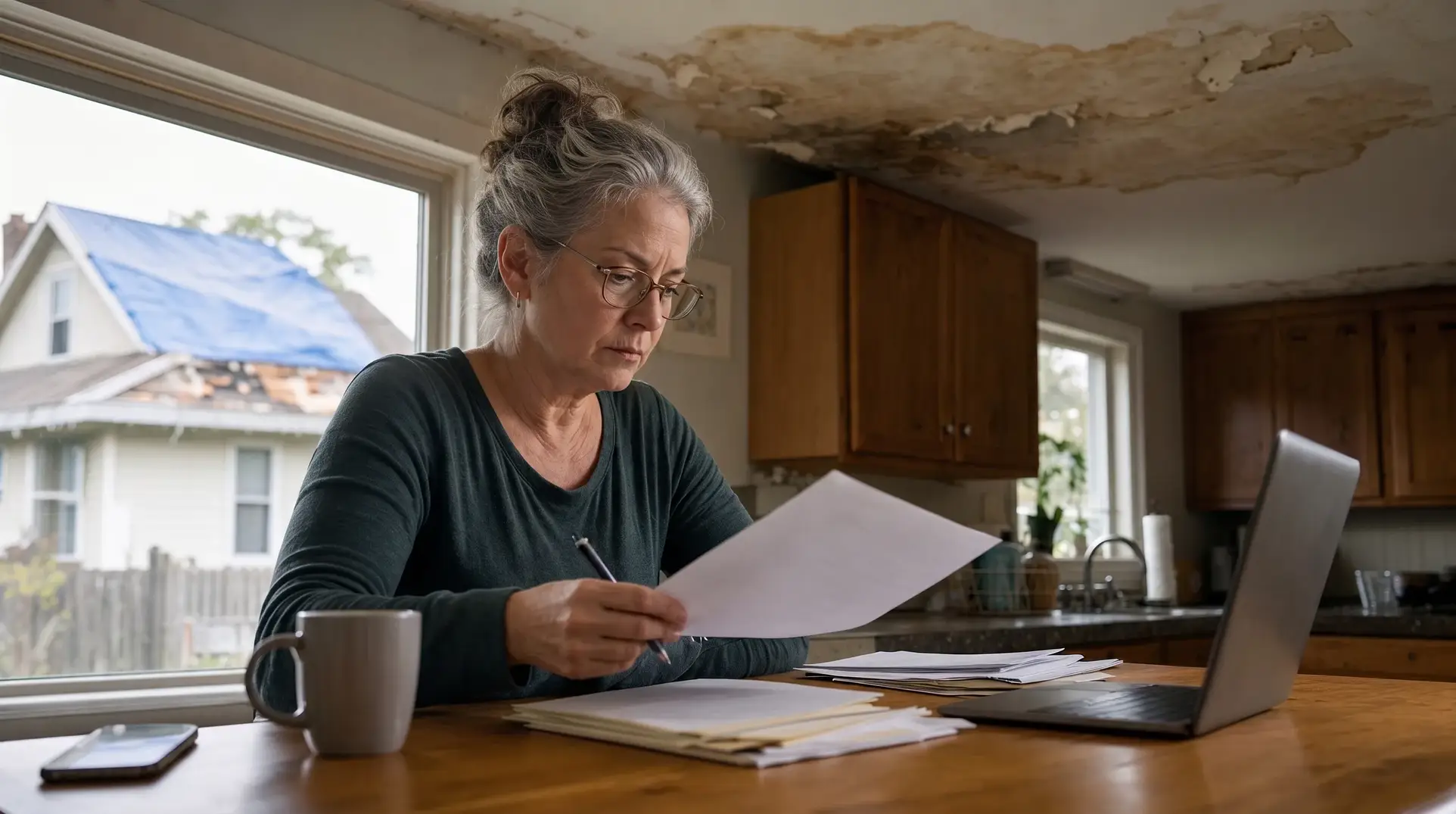

Severe thunderstorms caused about $45 billion in economic losses across the U.S. in just the first half of 2024, with more than $34 billion of it insured according to Munich Re, putting significant financial pressure on carriers and restoration professionals alike. For builders and restoration professionals, understanding how to navigate complex windstorm deductibles and policy limits is essential to protecting your scope of work.

Key Takeaways

- Industry Losses: Munich Re estimates U.S. severe thunderstorms caused about $45 billion in total economic losses in the first half of 2024, with more than $34 billion insured.

- Tornado Volume: A Texas tornado claims law firm, citing Insurance Information Institute data, reports Texas ranked first nationally for tornado activity in 2024, with 169 tornadoes recorded [1].

- Deductible Structures: Property owners may face separate windstorm deductibles calculated as a percentage of total insured value.

- Common Denials: Claims are frequently underpaid due to alleged pre-existing damage, unmet deductibles, or lack of evidence.

The Financial Pressures Driving Tornado Claim Underpayments

The restoration industry is facing a challenging environment as insurance carriers attempt to mitigate massive weather-related losses. Severe thunderstorms caused about $45 billion in economic losses across the U.S. in the first half of 2024, with more than $34 billion insured according to Munich Re, increasing financial pressure on carriers that can result in more rigorous scrutiny of claim estimates and coverage [4] [5] [2]. When carriers experience catastrophic losses across multiple regions, contractors often encounter heightened scrutiny of their estimates and increased pushback on coverage questions.

This pressure is particularly acute in high-risk areas. Texas has consistently ranked among the top states for tornado activity, and a Texas tornado claims law firm citing Insurance Information Institute data reports the state recorded more tornadoes than any other in 2024 [3]. For contractors and builders, this means that perfectly legitimate scopes of work are frequently challenged, delayed, or denied outright to protect the carrier’s bottom line.

Standard Policy Coverage and Windstorm Deductibles

Because aggressive claim-undervaluing tactics are directly tied to carrier losses, understanding the nuances of standard policy coverage is your first line of defense against underpayment. Standard commercial and residential property policies generally cover wind and tornado damage, but the specific application of deductibles can drastically alter the available funds for a restoration project.

Property owners in certain states may face separate windstorm deductibles that are calculated as a percentage of the home’s total insured value rather than a flat dollar amount. For example, a 2% windstorm deductible on a $500,000 property requires the property owner to absorb $10,000 before coverage applies. Contractors must identify whether a windstorm or hail deductible applies to the specific loss date and cause of loss, as miscalculating this figure can lead to unexpected out-of-pocket costs for the client and delayed payments for the builder.

The 3 Tactics That Impact Your Claim Recovery

Because underinsurance gaps and high deductibles commonly trigger adjuster disputes, recognizing the specific methods carriers use to reduce payouts is critical for protecting your project margins. Insurance companies often underpay tornado claims by citing pre-existing damage, unmet deductibles, lack of evidence, or failure to make temporary repairs [1].

1. Citing Pre-Existing Damage

Adjusters frequently attribute roof, siding, or structural damage to age, wear and tear, or previous storms rather than the recent tornado event. Contractors must counter this by providing clear, date-stamped photographic evidence of the property’s condition prior to the storm, alongside detailed weather reports confirming the tornado’s path and wind speeds at the exact property location.

2. Disputing Evidence and Temporary Repairs

Policies require property owners to mitigate further damage after a loss. Carriers often use a failure to make temporary repairs may result in reduced coverage or denial of coverage for additional damage that could have been prevented, but typically does not result in automatic denial of the entire interior water damage claim [1]. Conversely, if temporary repairs are made but the original damage is not thoroughly documented first, the adjuster may claim a lack of evidence. Restoration professionals must document every inch of damage before placing a single tarp.

3. Leveraging Complex Deductible Structures

As noted, unmet deductibles are a primary reason for claim underpayment [1]. Adjusters may incorrectly apply a percentage-based windstorm deductible when a standard flat deductible should apply, or they may separate damage into multiple claims with multiple deductibles. Contractors must carefully review the declarations page to ensure the carrier is applying the correct deductible structure for the specific weather event.

How Contractors Can Protect Their Scope of Work

Because carriers actively look for reasons to dispute evidence and temporary repairs, restoration professionals must adopt rigorous documentation and policy review standards. Relying solely on the adjuster’s interpretation of the policy language often leaves significant funds on the table.

Contractors should implement a standardized intake process that includes securing a complete copy of the property owner’s insurance policy, including all endorsements and exclusions [1]. That review should also confirm the policy’s named insured vs additional insured designations, since only parties properly listed on the policy have standing to be paid on the claim. By analyzing the exact policy language before submitting an estimate, builders can format their scope of work to align with covered perils and avoid common denial triggers. Additionally, establishing a formal partnership program with claim review experts allows contractors to identify underpayments early in the process, ensuring that complex policy language is interpreted correctly and that the full scope of necessary repairs is funded.

Frequently Asked Questions

Does standard property insurance cover tornado damage?

Yes, standard property insurance policies typically cover damage caused by windstorms and tornadoes. However, the extent of the coverage depends on specific policy limits, exclusions, and whether the property is located in a high-risk zone that requires specialized windstorm endorsements.

What is the difference between a flat deductible and a percentage deductible?

A flat deductible is a set dollar amount that the property owner must pay out of pocket before insurance covers the rest. A percentage deductible is calculated based on the total insured value of the property, meaning a 2% deductible on a $400,000 structure would require the property owner to cover the first $8,000 of damage.

Why do insurance companies deny tornado claims?

Insurance companies often underpay or deny tornado claims by citing pre-existing damage, unmet deductibles, lack of evidence, or failure to make temporary repairs [1]. Carriers may argue that the damage was caused by poor maintenance rather than the storm itself to avoid paying for a full replacement.

How can contractors prevent scope of work disputes?

Contractors can prevent disputes by thoroughly documenting the damage with high-resolution photos and videos before making any temporary repairs. Additionally, reviewing the property owner’s policy language ensures the estimate is written in a way that clearly aligns with covered perils and avoids common adjuster objections.

How to Secure Full Payment for Your Restoration Projects

Navigating tornado damage claims requires a proactive approach to policy analysis and meticulous documentation. By understanding the financial pressures driving carrier underpayments and anticipating common denial tactics, contractors can protect their margins and ensure their clients receive the funds necessary for a complete rebuild. Thoroughly reviewing deductible structures and policy limits before submitting an estimate is the most effective way to prevent costly delays. If your contractor claim was denied, JustClaims‘ AI reviews your policy language and flags underpayments before you dispute.

This content is for informational purposes only and does not constitute legal or insurance advice.

Sources

[1] https://carrigananderson.com/faqs/what-to-do-if-your-tornado-damage-claim-is-underpaid/

[2] https://www.eenews.net/articles/us-reels-from-45b-in-thunderstorm-losses-over-6-months/

[3] https://www.iii.org/fact-statistic/facts-statistics-tornadoes-and-thunderstorms

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. A licensed Public Adjuster in TX (#2125659), FL (#W455048), CO (#769172), and 10 additional states, Taylor founded his own firm before joining JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor's mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.