What Is a Claims Adjuster? Types, Roles & Valuation Methods (2026)

June 11, 2026

Written by Taylor Bezek

Share

When property damage occurs, claims adjusters evaluate the loss to determine if the insurance company must pay and what the appropriate settlement amount should be. For contractors and builders, understanding the different types of adjusters is essential for protecting your scope of work and keeping projects on schedule. Knowing who represents the insurer versus the property owner can significantly impact how a claim is valued and negotiated.

Key Takeaways

- Core function: Claims adjusters evaluate insurance claims to assess the insurer’s liability and determine the appropriate settlement amount.

- Independent adjusters: An independent adjuster is hired on a contract basis by an insurance company to represent the insurer’s interests during the settlement of a claim.

- Public adjusters: Licensed public adjusters are hired by policyholders to help settle an insurance claim on their behalf, though they cannot obtain more than the policy allows.

- Valuation methods: After an insurance company sends an adjuster to evaluate property damage, they determine a settlement amount based on either replacement cost or actual cash value.

Understanding the Claims Adjuster’s Role in Property Damage

Claims adjusters evaluate insurance claims to determine whether an insurance company must pay a claim and the appropriate settlement amount [1]. When a property owner files a claim for storm, fire, or water damage, the adjuster serves as the primary evaluator of the loss. For contractors, this means the adjuster’s assessment directly influences the approved scope of work and the funds available for reconstruction.

Their evaluation involves inspecting the physical damage, reviewing policy language, and applying coverage limits to the specific situation. The adjuster documents the scene, takes measurements, and compiles an estimate that the insurance carrier uses to issue the initial payout. Understanding how these professionals operate helps contractors set accurate expectations with property owners regarding timelines and budget constraints.

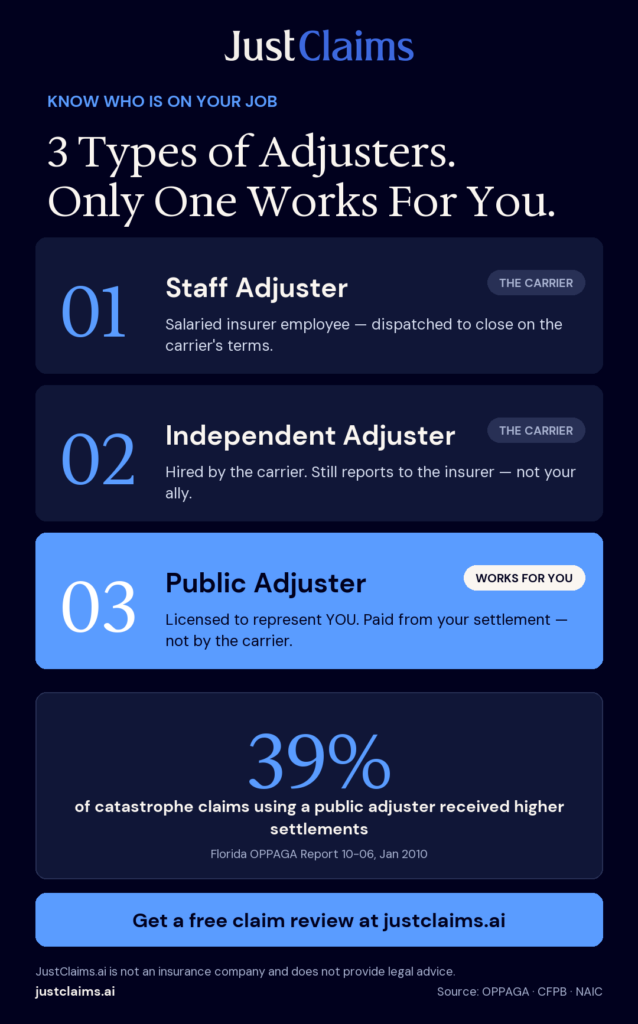

The 3 Adjuster Types That You Need to Know

Because the adjuster’s initial evaluation dictates the baseline for the project budget, knowing exactly who is inspecting the property is the first step in managing the claim process.

1. Staff Adjusters

Staff adjusters are direct employees of the insurance carrier. They are dispatched to evaluate damage and write estimates strictly on behalf of their employer. When interacting with a staff adjuster, contractors should remember that this individual’s primary directive is to align the settlement with the carrier’s internal guidelines and policy interpretations.

2. Independent Adjusters

During catastrophic weather events or periods of high claim volume, carriers often outsource inspections. An independent adjuster is hired on a contract basis by an insurance company to represent the insurer’s interests during the settlement of a claim [2]. While they do not work directly for the carrier as W-2 employees, their allegiance and reporting structure remain tied to the insurance company paying their fee.

3. Public Adjusters

Unlike staff or independent representatives, public adjusters work exclusively for the policyholder. Licensed public adjusters work for the insured — not any insurance company — to assist in the preparation, presentation, and settlement of the claim [3]. For contractors, collaborating with a public adjuster often helps bridge the gap between a carrier’s initial low estimate and the actual cost of construction, as the public adjuster advocates for the property owner’s financial recovery.

How Adjusters Value Claims and Determine Settlements

Since the type of adjuster assigned to a claim influences the negotiation dynamic, understanding the specific valuation methods they use is equally important for protecting your project margins.

Once the insurance company sends an adjuster and evaluates the damage, they pay a settlement amount based on the provisions in your policy — either actual cash value (which accounts for depreciation) or replacement cost value [4]. This distinction dictates how much money the property owner receives upfront and what documentation the contractor must provide to release withheld funds.

Replacement Cost Value (RCV)

Replacement cost policies are designed to cover the expense of repairing or replacing damaged property with materials of similar kind and quality at current market prices. Adjusters calculating RCV will not deduct for age or wear and tear in the final payout, though they often hold back depreciation until the contractor proves the work is complete.

Actual Cash Value (ACV)

When an adjuster applies an actual cash value settlement, they calculate the replacement cost and then subtract depreciation based on the age and condition of the damaged items. If a property owner only has an ACV policy, the initial payout is final, which can leave a significant funding gap for the required construction work. Contractors must verify whether the adjuster is applying RCV or ACV rules before finalizing contracts.

The 3 Inspection Steps That Matter for Contractors

Because valuation methods like ACV and RCV directly impact the available funds, contractors must actively participate in the inspection process to prevent missed damage.

1. Pre-Inspection Documentation

Before the adjuster arrives on site, contractors should thoroughly document all property damage with photographs, written descriptions, and itemized lists before or during the adjuster’s inspection to support the claim. This preparation supports the position that all necessary repairs are accounted for when the adjuster begins their evaluation.

2. On-Site Adjuster Interactions

During the physical inspection, contractors can walk the property with the adjuster to point out specific structural issues or code upgrade requirements. Maintaining a professional dialogue and providing manufacturer specifications or local building codes can help the adjuster justify a more accurate estimate to the carrier.

3. Post-Inspection Negotiations

After the adjuster submits their initial report, the carrier issues a statement of loss. Contractors must carefully compare this document against their own estimates. If discrepancies arise regarding material costs or missing line items, submitting detailed supplements with supporting evidence puts the carrier on notice that the initial settlement requires revision. Initial adjuster estimates may omit legally required safety measures and administrative costs such as permits and fall protection, making it important for contractors to review estimates carefully and submit supplements for any missing items. When an adjuster and the property owner still cannot agree on the value of the loss after supplements, the policy’s appraisal clause can force a binding valuation through independent appraisers and an umpire

Frequently Asked Questions

What is the main difference between an independent adjuster and a public adjuster?

An independent adjuster works on a contract basis for the insurance company and represents the carrier’s financial interests during a claim. In contrast, a public adjuster is hired directly by the property owner to advocate on their behalf and negotiate a fair settlement for the property damage.

How does an adjuster decide how much a claim is worth?

Adjusters calculate the value of a loss by inspecting the damage and applying the specific terms of the insurance policy. They typically determine the payout using either the actual cash value, which deducts for depreciation, or the replacement cost value, which covers the current market price of repairs.

Can a contractor negotiate directly with a claims adjuster?

Contractors can discuss the scope of work, material costs, and repair methods with an adjuster during the inspection or supplement process. However, contractors cannot legally negotiate policy coverage or act as a public adjuster on behalf of the property owner without the appropriate state license — and in many states, a licensed public adjuster is also prohibited from performing repair work on the same property. Laws vary significantly by state; contractors should consult a licensed attorney familiar with their jurisdiction before engaging in any claims advocacy role.

Why do insurance companies use independent adjusters?

Carriers frequently rely on independent adjusters when they experience a surge in claims, such as after a major hurricane, hail storm, or wildfire. Because these adjusters operate as contractors, they allow the insurance company to scale their workforce quickly without hiring full-time staff.

How to Protect Your Scope of Work

Navigating the insurance claims process requires a clear understanding of who is evaluating the damage and how they calculate the settlement. By recognizing the differences between staff, independent, and public adjusters, contractors can better prepare their documentation and set accurate expectations with property owners. Proper preparation helps demonstrate the true cost of repairs and reduces the likelihood of severe underpayment. If your insurance claim was denied or underpaid, JustClaims‘ expert team — accelerated by our bespoke AI — reviews the policy language, compares it against your documentation, and flags likely underpayments so you can go back to the carrier with confidence.

This content is for informational purposes only and does not constitute legal or insurance advice. Coverage decisions depend on the specific terms, conditions, and exclusions of each policy and the laws of the applicable jurisdiction; policyholders and contractors should consult with a qualified professional for advice on their particular situation.

Sources

[1] https://content.naic.org/sites/default/files/call_materials/Public%20Adjuster%20Model%20Comments.pdf

[2] https://content.naic.org/sites/default/files/call_materials/Public%20Adjuster%20Model%20Comments.pdf

[3] https://www.iii.org/article/what-public-adjuster

[4] https://www.consumerfinance.gov/ask-cfpb/how-do-home-insurance-companies-pay-out-claims-en-1523/

Taylor Bezek

As the General Manager at JustClaims, Taylor Bezek brings over a decade of experience managing complex residential, commercial, and large-loss claims. A licensed Public Adjuster in TX (#2125659), FL (#W455048), CO (#769172), and 10 additional states, Taylor founded his own firm before joining JustClaims to scale a tech-forward solution for the insured. He is committed to combining industry expertise with AI to enhance speed, clarity, and outcomes for every policyholder. Taylor's mission is to modernize the public adjusting profession and ensure owners get exactly what they are entitled to.